Arbidyne February Fund Newsletter

-

By InvestorHubFx

By InvestorHubFx - February 20, 2022

- InvestorHubFx Analysis

Feb 20th, 2022

The Arbidyne Absolute Return Fund implements a long/short investment process which aims to produce consistently positive returns in multiple market cycles. Our primary focus is USAn and US equities; and complement this strategy with global index futures, currencies and government bonds when opportunities present.

Net performance in January was 9.23%

Net performance since fund inception is 4.52%

Commentary

“The only thing that really matters in asset allocation is sidestepping some of the pain when the rare, great bubbles break.” – Jeremy Grantham

Global stock indexes suffered in January on the back of rising rate expectations and bond buying tapering, with the S&P 500 down -5.3% and the tech heavy Nasdaq down -8.5%. And as I write these comments today, the indexes have seen further weakness into February.

For the first time in history, the US is experiencing a confluence of three macro extremes all at once:

▪️ Enormous debt

▪️ Rising inflation

▪️ Excessive financial asset valuations

This combination of these factors is likely to weigh heavily on the US stock market indices going forward. This is good news for long/short style investors such as ourselves, but bad news for the traditional buy and hold.

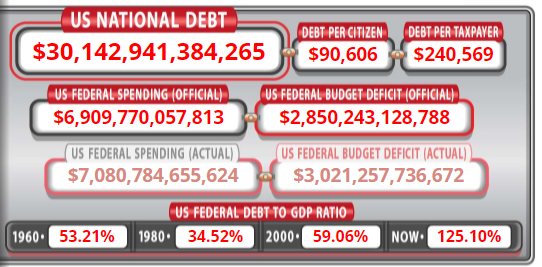

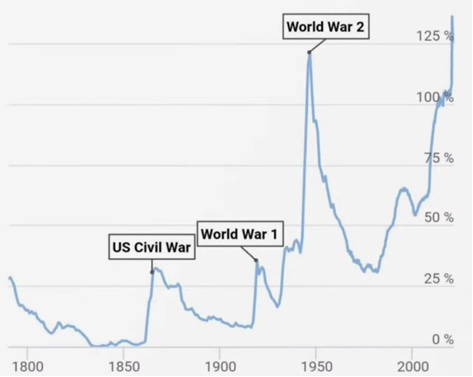

Notably, the US national debt breached the $30 trillion limit in January

Source: www.usdebtclock.org/

US debt to GDP now exceeds the peak made at the end of world war 2.

Inflation continues to rise, and is suggesting the Fed fund’s target rate will have to go much higher.

Where is the ‘Fed put’?

Regular reads will know we have been talking about this rising inflation problem for months, as the waves of stimulous money, child tax credits, PPP loans, and money printing were all pointing to much higher inflation. However, despite the fact that this explosion of inflation was obvious to all who cared to take the time to study, the Fed did not take action until inflation became a polical concern. It was only when inflation got so high that all the polls were showing voter concern about inflation that they decided to act. It thus follows that the fed is not going to act when the market declines until people start complaining. Which means indexes could continue to make new lows in the coming months.

The Safehaven Play

For a long time, the crypto space was eating gold’s lunch with talk that Bitcoin was the new digital gold. These last few months of risk off have seen the crypto space sell off sharply with Bitcoin down close to 30% year on year. Gold has been on the rise as shown in the chart below. And recently with the risk of Russian Invasion of Ukraine, we have seen gold up as Bitcoin sells, so itt seems that when it comes to finding a safehaven, Bitcoin is not digital gold, only gold is gold.

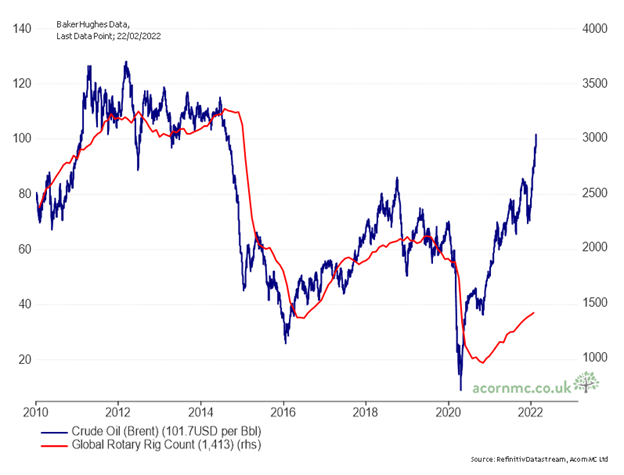

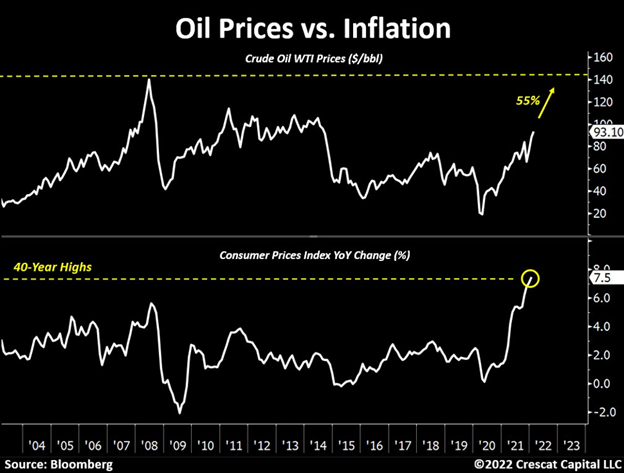

The coming oil super-spike

Oil prices have been on the rise, with prices almost back to US$100 a barrel. Normally higher prices encourage more drilling. However, with a combination of Environmental Social and Governance (ESG), the new Green agenda in Washington and perhaps Covid Labour shortages, the number of rigs drilling for oil is still lagging. If we then add in extra demand from everyone wanting to travel after all the covid restrictions over the last couple of years, we have the recipe for demand far outstripping supply in the near future.

Economics 101 states that when demand exceeds supply, prices will go up. The problem for the central banks is that higher oil prices could further exacerbate the already high inflation we are experiencing.

Source: Crescat Capital LLC

Thus, we believe Inflation is likely to remain high in the coming months. This is going to weigh on the Fed’s decision to raise interest rates in order to slow the economy down. With the market already off sharply from the highs, the indexes are likely going to experience more pain going forward. The good old days of the Fed being able to cut raise and add stimulus every time the market had a wobble are over, as this will just add more fuel to the inflationary fires that are currently raging.

It is not all bad news though. Bond markets have already priced in roughly 9 Fed rate hikes for the next two years. As rates rise and market wobbles continue, it is likely that some of these rate hike expectations will be trimmed back. Investment into green energy and renewables will continue, commodity prices will likely continue to strengthen.

Our aim is to grow your wealth whilst managing risk. Investing is a marathon, not a sprint and new opportunities in the market are always going to present themselves. Our aim is to find trades where the upside outweighs the downside, and then diligently execute our trade plans; profitable trades then tend to be a byproduct of this process.

If you have any questions or comments, please drop us a line at [email protected]

For new clients:

Since we are running individually managed accounts, new clients will not always have the same positions as our master tracking account when they first join, and as a result may not see the same monthly performance. This is because we cannot always buy new accounts into the same positions that were entered into before they joined the fund. We consider this on a case-by-case basis and evaluate whether it is in the individual client’s best interests to enter into existing positions. New accounts should see their accounts begin to track our performance benchmark approximately 3 months after joining.

DISCLAIMER: This information has been prepared by Arbidyne Pty Ltd.. This information is general in nature and nothing in this letter should be considered investment advice. The commentary reflects Arbidyne’s views and beliefs at the time of preparation, which are subject to change without notice. No representations or warranties are made by Arbidyne as to their accuracy or reliability. To the extent permitted by law, no liability is accepted by Arbidyne for any loss or damage as a result of any reliance on this information.

Related Posts

Why Has the Bank of England Resumed QE Despite Pound’s Plunge to Record Low?

- By InvestorHubFx

- October 5, 2022

Who Prevails in Strong Verse the Weak… Traders Do

- By InvestorHubFx

- January 18, 2024

Normalised Pricing versus Pricing Extremes in Forex

- By InvestorHubFx

- May 3, 2023